Latin America's Recovery from the Depth of the Pandemic Continues

Latin America continues its economic recovery from Covid-19, writes Pollyanna de Lima, Economics Associate Director, Economic Indices, IHS Markit...

Latin America continues its economic recovery from Covid-19, writes Pollyanna de Lima, Economics Associate Director, Economic Indices, IHS Markit

Latin American nations continued to recover from the pandemic-induced contractions seen in the first half of 2020, with GDP often beating forecasts. Growth prospects are now brighter given the rollout of vaccines, but still high numbers of COVID-19 cases and virus mutations threaten the near-term outlook. Although key countries in the region came out of technical recessions, output, employment and business investment remain below pre-COVID levels.

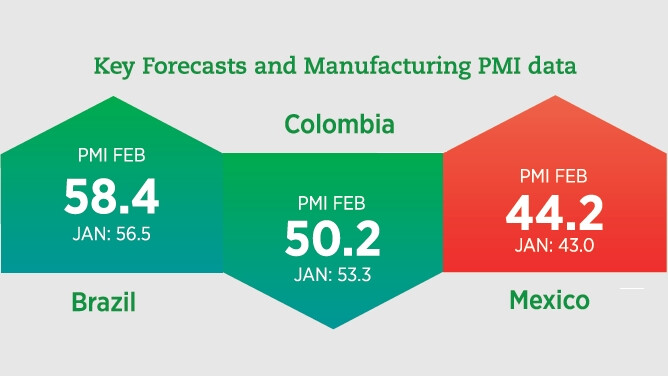

Macroeconomic PMI data, compiled by IHS Markit, pointed to divergent trends across the region at the start of 2021. Factory orders, production and employment in Brazil increased at quicker rates in February but, with services heavily impacted by the pandemic and national restrictions, private sector sales and output declined marginally. The Colombian manufacturing industry, where a notable pick-up in growth was registered at the start of 2020, experienced a setback in February due to the reintroduction of controls aimed at curbing the spread of the virus. In Mexico, the downturn in factory orders and production remained sharp, despite easing through the first two months of the year. Business confidence, however, improved across the board.

One area of concern, and a common theme, highlighted by the PMI surveys was the ongoing detrimental impact of supply chain distortions on companies’ expenses and profitability. Input costs continued to increase sharply, with only Brazilian firms able to retain some pricing power and pass on a substantial part of these additional cost burdens to clients. In the January economic outlook update, the IMF revised higher 2021 GDP projections for Brazil (+3.6%), Colombia (+4.6%) and Mexico (+4.3%) on the assumption that effective vaccine rollouts could boost confidence, consumption and investment. The forecast for Argentina was downgraded to +4.5% owing to COVID-19 challenges and fiscal constraints.

Brazil

Economic activity in Brazil expanded 3.2% in Q4 2020 from Q3, but closed the year with a record reduction in GDP (-4.1%). The IMF had anticipated a contraction of 5.8% last October and currently forecasts growth of 3.6% in 2021. While the quarterly average of the PMI Composite Index pointed to a solid rise in business activity in Q4 2020, monthly falls have been recorded since the turn of the year. Growth in the manufacturing industry softened in January and recovered some lost ground in February. However, a spike inCOVID-19 cases and the reintroduction of restrictions caused back-to-back declines in services activity. Nevertheless, business confidence strengthened in both segments during February as firms hoped that greater vaccine availability will be successful in curbing the disease and result in controls being lifted.

The official unemployment rate remains elevated, though fell for the third successive month in December to reach 13.9%. The PMI Employment Index highlighted renewed job shedding in the private sector as companies sought to keep a lid on expenses in light of steep cost increases caused by material shortages. The central bank has kept the policy interest rate at a record low of 2% to aid the recovery, but inflationary pressures will likely underpin the start of a tightening cycle in the first half of 2021.

Colombia

The Colombian manufacturing industry experienced a mild fall in output during February due to tighter COVID-19 controls, according to the Davivienda PMI compiled by IHS Markit, after growth had gained momentum in January. Inflows of new business declined, but companies lifted employment amid upbeat sentiment regarding the 12-month outlook for business activity.

"he IMF revised higher 2021 GDP projections for Brazil (+3.6%), Colombia (+4.6%) and Mexico (+4.3%) on the assumption that effective vaccine rollouts could boost confidence…"

Official data pointed to a 6.0% quarterly rise in economic activity in Q4 2020, and a softer-than-expected reduction of 6.8% for the year as whole. The IMF forecasts growth of 4.6% in 2021 and 3.7% in 2022. Domestic consumption could receive a boost from rising employment once companies start to replace staff laid off due to the COVID-19 crisis. The official unemployment rate remains high (17.3% in January), but is some way below last year’s peak of 21.4%. Marginal job creation was signalled by goods producers in the PMI panel during February.

Mexico

Official data indicated that Mexico’s economy shrank 8.2% in 2020. Looking ahead, the IMF expects economic activity to bounce back by 4.3% in 2021 as the country recovers from the pandemic-induced contraction, then growth to slow to 2.5% in 2022. February PMI data indicated that the Mexican manufacturing industry continued to struggle. New orders, and production decreased at slower rates that were nevertheless sharper than any recorded before the COVID-19 crisis.

Subdued demand and ongoing increases in input costs led firms to trim employment for the thirteenth month in a row. Business optimism strengthened, however, owing to vaccine developments. Despite upward inflationary pressures, the central bank reduced the policy interest rate to 4.0% in February — the lowest since May 2016 — in an attempt to revive the economy.

Argentina

Economic conditions in Argentina remain challenging as a result of high debt, currency instability and elevated inflation. Parallel to this, COVID-19 restrictions continue to restrict consumption. Fiscal stimulus and monetary policy meant to support the economy are restricted by a spike in the fiscal deficit and hyperinflation. In 2020, consumer price inflation was at 36% and markets expect it to exceed 40% in 2021.

The official interest rate is currently at 38%, while the Argentinian peso (vs USD) has depreciated by some 45% over the past year. The unemployment rate was at 11.7% in Q3 2020. While there were upward revisions to 2021 GDP forecasts in other LATAM nations, the IMF lowered the prediction for Argentina. Gross domestic product is now expected to expand by 4.5%, compared with a forecast of 4.9% last October. For 2022, economic activity is predicted to rise by 2.7%.