Interview with Adrián Armas, General Manager of the BCRP’s Economic Study Centre

We sit down with, Adrián Armas, General Manager of the BCRP’s Economic Study Centre, to understand how Peru’s central bank manages one of Latin America’s most stable economies…

This interview is part of our Latin American central bank special report…

What are Peru’s economic strengths?

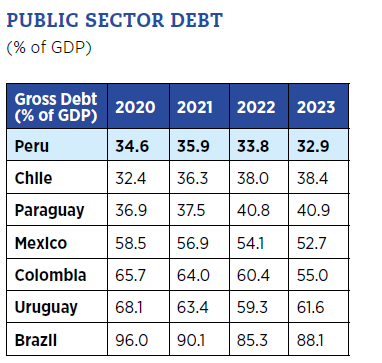

Adrián Armas: Peru has long enjoyed a political and social consensus on maintaining a robust macroeconomic framework, characterized by low fiscal deficits and minimal public debt. Consequently, Peru boasts one of the lowest debt-to-GDP ratios globally. This fiscal discipline, coupled with the constitutionally guaranteed independence of the Central Reserve Bank of Peru (BCRP), mandated to ensure price stability, fosters a conducive environment for responsible monetary policy. For instance, the BCRP is legally forbidden from lending money to the government.

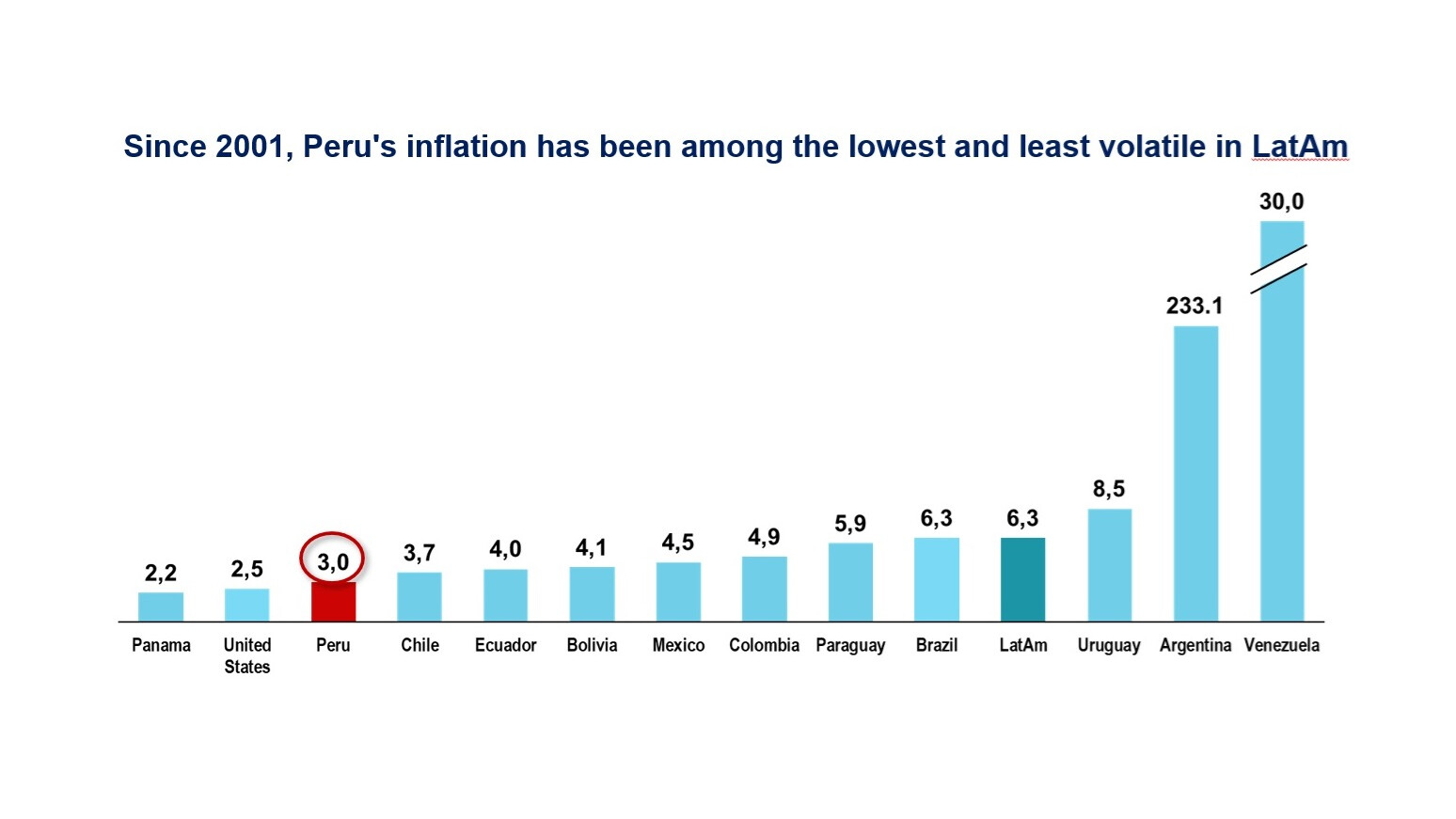

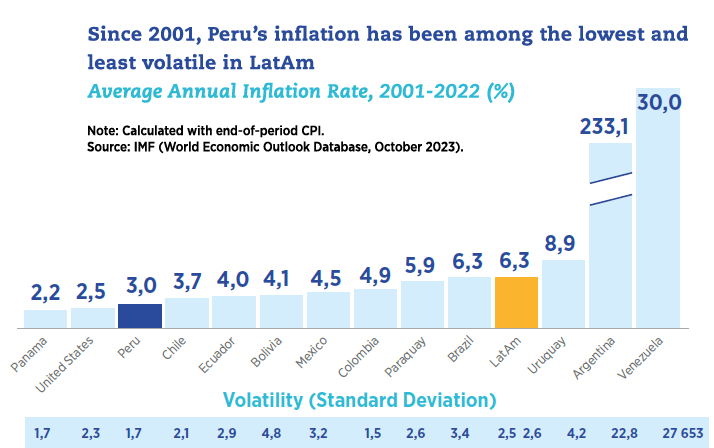

Peru has the distinction of having the lowest inflation rate among Latin American countries with their own currency, averaging 3% annually since the turn of the century. Only Panama, where the dollar is the official currency, has experienced a lower rate, while inflation in the U.S. averaged 2.5% annually from 2000 to 2022.

Why have most Latin American banks been so successful at controlling inflation?

AA: At present, tackling inflation tops the BCRP’s agenda. Encouragingly, inflation has been on a downward trend, notably since June 2023. By September, Peru’s inflation rate stood at 5.0%, with core inflation at 3.6%. I believe Latin America’s extensive history of grappling with inflation has equipped central banks in the region to respond swiftly this time around. Our counterparts across Latin America promptly escalated policy rates, fully aware of the danger posed by inflation. It is fair to say that the inflation-targeting (IT) regimes adopted by countries like Guatemala, Mexico, Colombia, Peru, Chile, Paraguay, Uruguay, and Brazil, have proved effective.

Is the BCRP worried that El Niño will stoke inflation?

AA: Indeed, in our most recent monetary policy statement, we expressed concerns over the potential price impacts of this weather phenomenon. However, I believe it won’t entirely reverse the progress on inflation mitigation. Peru has weathered multiple supply shocks in recent years, including political instability, disruptive protests, and soaring fertilizer prices due to the conflict in Ukraine. While these shocks are now subsiding, new ones tied to El Niño might arise.

Inflation in Peru peaked in June last year at 8.8%, while the U.S. hit a high of 9.1% concurrently. However, by May of this year, inflation in Peru had only decreased to 7.9%, compared to 3% in the U.S., indicating that we benefited less from the easing of food price shocks than other economies. Yet, since May, the decline in Peru’s inflation has been more significant, currently standing at 5.0%.

In light of this, the BCRP’s monetary policy statement in August removed the mention of potential new policy rate hikes. In September and October, the BCRP cut the policy rate by 25 basis points each month. The statement clarified that future adjustments don’t necessarily have to follow a consecutive sequence of reductions, and that any new adjustments will be data-driven.

Does the BCRP intervene in the FX market?

AA: When Peru transitioned to an IT regime 21 years ago, the aim was to empower the BCRP to implement monetary policy using a policy interest rate. However, to avoid high interest rate volatility, central banks require an additional instrument. Unlike other Latin American nations such as Mexico, Chile, and Colombia, we operate in a financially dollarized economy, exposing us to potential vulnerabilities if unexpected domestic currency depreciation adversely impacts borrowers with dollar debts and local currency incomes.

The solution lies in FX intervention, not to fix the exchange rate at a particular level, but to reduce its volatility. BCRP initiated this policy in 1990, well ahead of other countries in the region. To intervene in the FX market, a substantial level of international reserves is required, which is why Peru currently holds more than $70 billion in hard currency—roughly equivalent to 30% of GDP. This buffer enables the BCRP to implement a counter-cyclical policy and mitigate the impact of economic shocks.

Observing the value of the Peruvian sol (PEN), it’s evident that this policy has been effective. The PEN follows the trend of other regional currencies, albeit with less volatility.

Is there a certain minimum level of international reserves that Peru needs to guarantee macroeconomic stability?

AA: Obviously, the scale of our intervention depends on the size of the shock, but there isn’t a specific threshold of concern. This century, Peru has been hit by several shocks. We had the Great Financial Crisis in 2008, then the end of the commodity super-cycle in 2013. The biggest came with the wave of political uncertainty in 2021, when capital outflows from Peruvians moving money abroad reached almost 8% of GDP. The BCRP intervened during each of these instances, yet the overall reserve level never fell abruptly.

The strength of the BCRP’s approach lies in its aim not to peg the PEN at a specific level, but rather to smooth out exchange rate fluctuations. By intervening in a floating exchange rate system, the BCRP lessens susceptibility to speculative attacks. The risk of rapid depletion of international reserves arises when a central bank attempts to defend a fixed exchange rate, as exemplified by the Bank of England during the Black Wednesday event in 1992.