Green Shoots of Recovery in Latin America

The region is bouncing back from the depths of the Covid-19 economic crisis, writes Pollyanna De Lima, Economics Associate Director Economic Indices, IHS Markit...

The region is bouncing back from the depths of the Covid-19 economic crisis, writes Pollyanna De Lima, Economics Associate Director Economic Indices, IHS Markit...

Although most economic indicators for Latin America show that contractions associated with the coronavirus disease 2019 (COVID-19) pandemic bottomed out amid the loosening of restrictions aimed at halting the disease, a spike in fatalities and cases threatens the recovery as tighter controls could be implemented. Business investment remains subdued amid concerns towards the outlook and the labour market continues to suffer, with firms likely to keep a lid on expenses in the near term.

Timely PMI data, compiled by HIS Markit, showed notable progress across a number of key measures once lockdown restrictions had been lifted. Improved trends for economic activity and demand had been registered in October, but uncertainty towards growth prospects and cost-saving initiatives meant that businesses remained reluctant to lift employment. At the same time, companies generally saw their expenses increase further, with currency weakness, material shortages and the purchasing of hygiene products and personal protective equipment pushing up inflation.

October saw the International Monetary Fund (IMF) revise downwards their predictions for GDP in 2020 as the negative impacts of the COVID-19 pandemic were reassessed. With levels of economic output expected to be lower than initially estimated, forecasts for 2021 have generally been adjusted upwards. While fiscal stimulus aimed at reinforcing the recovery and protecting the most vulnerable has been welcomed, concerns about public debt mounted.

Brazil

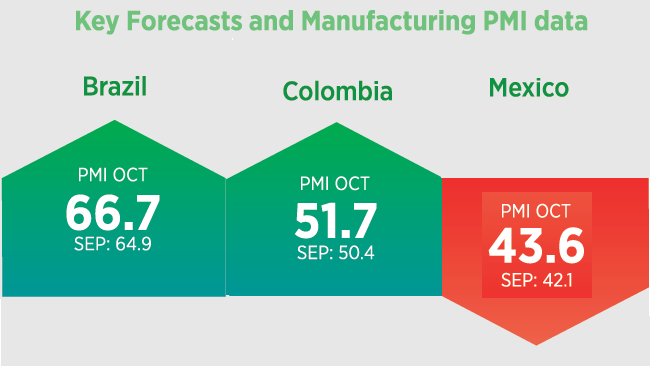

Despite seeing one of the highest numbers of COVID-19 deaths and cases globally, relatively softer restrictions across Brazil meant that economic conditions improved during October. PMI data showed that the service sector joined its manufacturing counterpart in posting output growth during September, with the recovery of the latter starting in June. Since rates of increase accelerated in October, private sector activity expanded at the strongest pace in over a decade. Caution needs to be taken when interpreting the results as data measure monthly, rather than annual, changes and output levels had reached rock bottom at the onset of COVID-19.

The IMF forecasts a -5.8% reduction in 2020 GDP and the unemployment rate, currently at 14.4%, to settle at 13.4%. To support the economic recovery, Brazil’s Central Bank kept its policy interest rate at a record low of 2% in October, despite signs of intensifying inflation. Fiscal stimulus has been extended, with the government reporting R$587.5 billion in new debt linked to measures aimed at limiting the economic and social impacts of the pandemic.

Argentina

The IMF reported a sharp downgrade in its 2020 GDP forecast for Argentina as the deep recession the country is in was exacerbated by the COVID-19 pandemic. Gross domestic product is anticipated to shrink by -11.8%, the sharpest rate across Latin America. Official data showed a steep annual decline of -19.1% in GDP during the second quarter, which compared with -5.2% in Q1. Concurrently, the unemployment rate exceeded 13%.

The Central Bank of Argentina lowered its benchmark interest rate to 36% in October, which had been unchanged at 38% since March and compared with 68% one year ago. The peso continued to depreciate over the month and was -32% down against the US dollar since the start of the year, as of November 5th.

Colombia

Following a prolonged lockdown period, Colombia started to see controls being lifted in September, which supported the tentative economic recovery signalled by high-frequency indicators. The Davivienda Colombia Manufacturing PMI, compiled by IHS Markit, indicated that a renewed increase in sales underpinned production growth during October and companies resumed hiring efforts following a six-month period of job shedding. The monthly uptick in employment was marginal at best, however, and followed record reductions earlier in the year. Official statistics highlighted an unchanged unemployment rate of 15.8% in October that was the joint-lowest since March.

The PMI survey also showed that goods producers saw a further sharp increase in input costs, which they associated with supply shortages and currency weakness. Colombia’s Central Bank has reduced interest rates steadily since the pandemic hit. Rates were left unchanged at 1.75% in October, with the bank stating that historically low interest rates and fiscal support for households and firms are supporting the economic recovery.

Mexico

Mexico’s economy continues to be negatively impacted by the COVID-19 pandemic. GDP contracted by -17.1% in the second quarter compared with Q1 and shrank by -18.7% year-on-year. In contrast to the recoveries seen elsewhere in Latin America, the latest IHS Markit PMI indicated that the Mexican manufacturing industry remained entrenched in contraction.

October data showed sharp reductions in factory orders, exports, output, input purchasing and employment. Rates of decline were much softer than noted at the height of the pandemic, but remained stronger than any seen prior to the COVID-19 outbreak in the near ten-year survey history. Firms further lowered selling prices in efforts to stimulate demand, but this led to pressure on profitability amid an upsurge in cost inflation.

Having previously predicted a -6.6% contraction in 2020 GDP, the IMF now foresees a -9.0% fall. In September, the Bank of Mexico cut interest rates to 4.25% – the lowest in four years – as part of ongoing attempts to support the economy.