Golden times ahead?

A strange divergence in the gold market suggests the yellow metal may have lost its shine but not its long-term value...

Gold is on a dismal losing streak. The seven straight months of losses until October was the longest such run since the 1960s. That statistic would mean a lifetime for some asset classes but it is just a blip in gold’s history of thousands of years. Commentators who talk of ‘unprecedented crises’ would be surprised at how often wars, recessions and even pandemics happen in human history. The one constant through all those cycles is gold. For thousands of years, it has kept its value as empires rose and fell.

But one thing gold did not have to deal with in ancient history is exchange-traded-funds. Today there is a strange divergence in the gold market. Financial investors are abandoning gold in the search for higher yields in an era of rising interest rates. But central banks and retail investors are buying record amounts of physical gold, no doubt spurred by worries about the colossal amounts of debt weighing down on fiat currencies. Meanwhile gold miners are caught in the crossfire – getting paid a lower price per ounce while inflation pushes their costs ever higher.

Financial flight

“Gold falls to 2-year low on US rate rise fears” screamed a recent headline in the financial press. The Federal Reserve tightening is definitely bad news for gold. As the benchmark rate rises, it increases the cost of credit throughout the economy and encourages investors to find higher-yielding assets. That has had a direct impact on the gold market, where gold-backed ETFs have seen five consecutive months of outflows. Indeed, during the third quarter, investors withdrew $12billion from gold-backed ETFs – the largest quarterly amount since 2013. According to the World Gold Council (WGC), investment levels in financial gold assets were down 47% year-on-year.

With Fed rates between 3.75% to 4% and long-term inflation expectations just under 3%, there is a strong incentive for investors to move their money into anything yielding more than 3%. However, were that to change. Let’s say for instance, that the current inflation rate of 7.75% were to prove more stubborn than current expectations and last for a decade, then we would have negative real interest rates and a strong incentive for investors to move capital out of paper assets that were losing their inflation-adjusted value every year.

Physical gold

It seems that retail investors are more worried about the second scenario. WGC figures showed that total retail demand rose 36% compared to the same quarter last year. Gold demand has now recovered to pre-pandemic levels after lockdowns in 2020 reduced gold demand to the lowest record on levels. In the UK that demand is reflected in the profits of the Royal Mint, which makes gold coins. Profits are up 50% as British investors clamour for physical precious metals. Indeed, gold is performing well when measured in sterling, and has proved a safe haven for local investors trying to protect themselves from the currency’s post-Brexit malaise.

Financial investors often move automatically in response to interest rates but retail investors make intuitive judgements about what they think will happen in the world. Time will tell who has made the right call but it’s interesting to see that central banks are also on a gold-buying spree. Central banks bought 400 tonnes of gold in the third quarter, which was a record high. Many analysts believe that more secretive countries, say Russia or China, are buying far higher amounts than officially recorded. In one way, the central banks are just like the high street consumer – they worry that the huge amounts of US government debt, which increased dramatically during the pandemic, will undermine the value of the US dollar.

But some central banks have another motive. The weaponization of the US dollar as an instrument of war against enemies, such as Iran and Russia, ultimately debases the value of the currency. Gold, especially physical gold held in a country, is proving more useful to Russia than dollar-denominated paper assets.

Mining the yellow metal

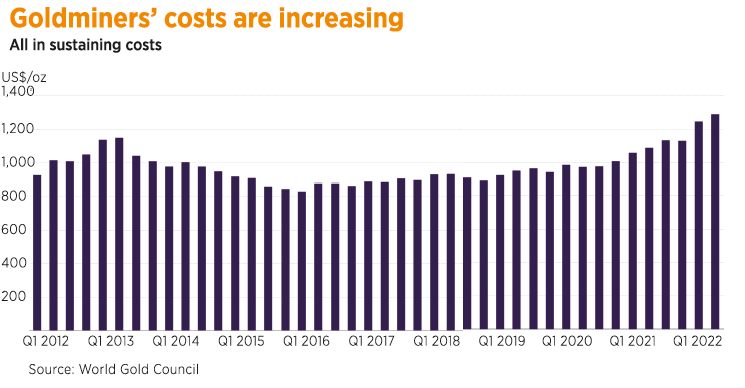

In the short-term, it is the goldminers that are suffering. The financial outflows are forcing down the price miners receive per ounce of gold. Meanwhile inflation is increasing mining costs. In particular, key petrochemical inputs, such as fuel, cyanide and explosives have risen sharply. Metals Focus, a consultancy, estimates it now costs gold miners an average of $1,693 to produce an ounce of gold. That figure, which includes financing and tax costs, is a 6% increase on 2021. With gold at around $1,780 at time of print, the higher costs don’t leave much room for earnings.

Falling profit margins could force consolidation in the mining industry. An early taste of that was the bidding war for London-listed Yamana Gold, with a joint offer from Agnico Eagle and Pan American Silver beating an earlier proposal from Gold Fields.

Another outcome of the profit squeeze is that mining companies are cutting back on exploration and greenfield development in an attempt to control costs. With miners not finding or developing new deposits, production will fall. That is already happening in Latin America. In the second quarter of 2022, output from the region’s ten-largest gold mines was down 5% compared to the same period in 2021.

These might sound like depressing trends for the industry but eventually they will be positive for the gold price. Some gold producers will already be unprofitable at current prices. If prices keep falling it will cause some mines to close, further restricting production. That will lead to a gold shortage, that will support higher prices in the future. Investors should take advantage of the current sell-off to find low-cost producers that have large deposits with expansion opportunities.