Can Argentina fulfil its renewable energy potential?

The country has incredible solar potential in the north and wind potential in the south but so far progress has been limited. Ezequiel Fernandez from Balanz Capital, investigates the opportunities for investors…

The country has incredible solar potential in the north and wind potential in the south but so far progress has been limited. Ezequiel Fernandez from Balanz Capital, investigates the opportunities for investors…

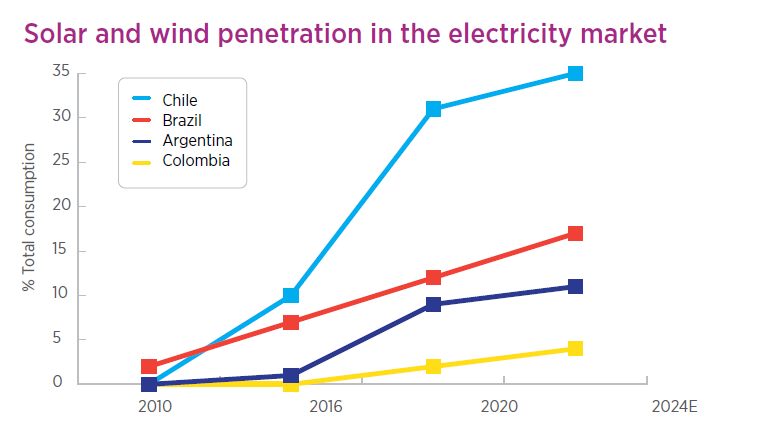

Argentina started its first serious push for renewable power in 2016, under the auspices of the Renovar 1.0 auction launched by the Macri administration. At the time, solar and wind power accounted for less than 1% of Argentina’s installed capacity, while solar and wind power in Chile was already at around 10%, at 8% in Brazil and 7% in Mexico. Thanks to further Renovar rounds, Argentina progressively started to catch up and the government also started to foster an unregulated green PPA market for private players called MATER.

Things were advancing fine until the 2019 macro-political crisis arrived and several renewable projects - even those with inked contracts and start dates already committed - experienced difficulties in finding financing. Hence, momentum was lost and project cancellations multiplied. By the time the pandemic hit, renewable penetration was standing at 5% and we were once again considerably trailing our Latin American counterparts despite above-average wind resource in Patagonia and world-class solar conditions in the northern provinces, only rivalled by Chile’s Atacama Desert.

Renewable objections

As the country emerged from the pandemic, some key infrastructure projects were progressively resuscitated. Nonetheless, there were limited hopes among energy companies that the Alberto Fernandez administration would resume the renewable power agenda. Historically, the Kirchner/Peronist alliance has been reluctant to foster higher penetration of renewables, despite ever decreasing development costs for solar wind projects. Renewable power auctions across the region saw prices as low as ~US$30/MWh - less than half what the Argentine government was paying for electricity and fuels on its subsidy scheme. So, why didn’t the government want more solar and wind projects?

There are three main reasons, in our view. The first one is related to employment levels, as the construction of large thermal facilities involves the employment of thousands of low-skilled workers during a construction phase, which can last two to four years. Renewables are less labour intensive and are built more quickly. The second reason relates to the future gas demand associated with the operation of the thermal power plants. This serves the further development of Vaca Muerta, it facilitates the construction of ancillary infrastructure that can be used for additional projects. Right or wrong, developing Vaca Muerta even at high costs has been a long-standing ambition of the ruling coalition, with the added benefitted of helping in getting them the political support of the hydrocarbon-rich Patagonian provinces in Congress.

Finally, we have the issue with the high-tension lines. Thermal power plants require relatively cheaper and simpler investments in transmission lines than renewables, mainly because a thermal plant can concentrate a lot of capacity in a single place and its location is not bound by resource conditions. Transmission costs are not expensive in average US$/MWh values when considering the extremely long useful life of the assets, but unlike in the rest of Latin America, the development of high-tension lines in Argentina is mostly carried by national state. A robust and resilient transport grid is a must for achieving high levels of renewable penetration but achieving that would increase Argentina’s public works budget, which is always running short of cash.

Renewable Solutions

The three arguments that we mentioned in favour of thermal do make some sense, but the neglect of renewable development comes at the cost of higher electricity bills for end consumers and environmental pollution. Regarding efficiency, thermal advocates generally bring forward the topic of renewable intermittency. After all, it isn’t fair to directly compare the energy price of a thermal plant, which produces reliable quantities of power, with the price offered by a solar farm, which provides an intermittent supply of electricity. The direct comparison is nonsensical, but government planners and regulators understand this very well and that is why they apply a formula to fix this trade-off between firm supply and cheaper costs.

Ultimately, it is all about finding that optimal mix between the two technologies. The most widely used tool to resolve this is “capacity-efficient modelling”. This entails building an optimisation model that includes all the associated costs, expected hourly output for each technology and system constraints. Such model tells the regulator if it is possible to add cheap renewables and help further with systemic costs or whether some additional thermal backup to make the grid more stable/secure is needed. Each expert has its own model and results may vary, but there is a big consensus that advances in low carbon technologies have allowed for very high share of renewable penetration without sacrificing security of supply. This is the basic tenet behind the ambitious pledges of achieving 80%, 90% or even 100% renewable power penetration that we have seen developed counties make.

A conservative version of our efficiency capacity model for Argentina tells us that even with gas prices as low as US$3.0/MMbtu (25% of what the UK currently pays for imported LNG), Argentina’s ideal power system would see 70% of electricity generated by a mix of hydro, solar and wind. This implies that current thermal power output in Argentina would be halved. Importantly, such calculation does not even include carbon costs. If we were to include the current CO2 price of US$100/tn in the European ETS market or factor-in the expected technical improvements in electricity storage solution such as advance lithium-ion batteries, the role of thermal would be diminished further.

Will a new Argentine administration change the optic and gear more aggressively towards solar and wind at some point in time? In the long run… yes. Beyond political considerations, the global trend is unstoppable and backed by economic factors. Argentina might even be forced to accelerate renewable adoption if cross-border carbon adjustments are implemented at national trade levels. Nonetheless, we will continue to lag in the short-term. Partly for the political reasons but also because most Latin America’s renewable energy growth is being driven by the large global energy holdings that exited Argentina in the last twenty years. Without private sector commitment and conviction, it is hard to implement a fast energy transition.