Buy Brazilian bargains

Our man in Brazil, Adam Patterson, analyses the investment and asset valuation outlook in Latin America’s largest economy…

Our man in Brazil, Adam Patterson, analyses the investment and asset valuation outlook in Latin America’s largest economy…

So far 2023 has been a bad year for the Brazilian economy. Local capital markets have been volatile while economic indicators are starting to point downwards. This is a sharp contrast from the positive economic progress seen under the market-friendly government of former president Jair Bolsonaro, who rules from 2018-2022. The new administration, headed by Luiz Inácio Lula da Silva, has shifted economic policy leftwards – tax and spend is back – and the market has taken note.

Macroeconomic challenges

The IMF expects Brazil’s GDP to grow by just 1% in 2023, while job creation fell by 38% in the first quarter. The fiscal deficit in March was the worst since the pandemic hit in 2020. Consolidated public sector debt is projected to almost double to 8.2% of GDP this year, whilst total debt as a percentage of GDP is expected to reverse the improvements of the last two years and increase to 75.8% in 2023, up from 72.9% of GDP in 2022. Moreover, after a ‘best in class’ monetary policy that significantly reduced inflation in 2022, prices are again rising.

Brazil´s stock exchange, the Ibovespa, is down around 6% since the presidential elections in October at the time of writing. The government´s proposed “fiscal framework” has not yet settled nerves. Needless to say, Brazilian valuations have dropped.

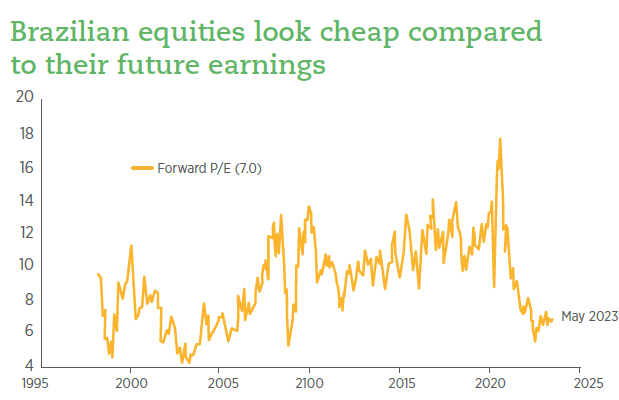

Brazilian bargains

Based on data from Yardeni Research, a global investment consultancy, the forward price-to-earnings (p/e) – a key valuation metric which divides the current share price of a company by the estimated future (“forward”) earnings per share (EPS) – for Brazilian listed equities is currently at 7, around 35% below its historical ten-year level of close to 11.

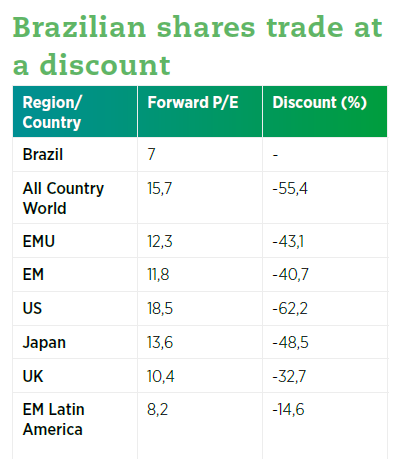

Brazil looks cheap compared to other international markets too. Brazil forward p/e ratios are 55% below the global average, 62% below US valuations and 33% below UK market prices. There is even a 15% discount when benchmarked against the Latin American average. Macroeconomic challenges, geopolitical worries and exchange rate risk are all weighing on investor sentiment. But the low valuations imply that investors are being compensated for these political, economic, and fiscal risk factors. Now the bargain basement prices are attracting investors and generating deals.

International optimism

In local currency terms, Brazilian stocks provided some of the best returns amongst major markets in 2022 - the MSCI Brazil index increased by 14% - as the Central Bank´s aggressive rate rises created a future scenario of lower rates – potentially, and eagerly, expected in the second half of the year - which could help boost economic activity and equity investment. Currently at 13.75%, the benchmark rate is at its highest since 2015. The median forecast for the end of year is 10.5%, with more conservative estimates at 12%. XP Inc, one of Brazil´s largest investment managers, expects the Ibovespa to close the year on 125.000 points, a 10% uptick from current pricing. According to Bloomberg, “foreign investors were also a major driver of 2022´s equity market rally, purchasing a net $19billion worth of Brazilian stocks, the most since records began in 2009”.

Despite the gains so far, there could be more to come. Brazil still benefits from a relatively cheap currency – attractive for global investors – and should also see some upside as China, its largest trade partner, slowly reopens. The US should also see peak interest rates this year, boosting the global carry trade. And of course, the country also benefits from its profile as a large, westernized, emerging economy with a solid legal system. As is often the case, international investors are more optimistic than domestic ones.

Britain buys Brazil

In the first half of 2022, PE investment reached R$16.5billion, an increase of 617.4%, according to the Brazilian Association of Private Equity and Venture Capital. Brazil was the third-largest global destination for foreign direct investment in 2022 as per OECD estimates. The country received $85billion, behind on the United States ($318billion) and China ($180billion).

UK companies were particularly prominent. Total (and UK overseas territories) foreign direct investment in Brazil in the 20 years to 2019 was $74billion, making it the third-largest international investor behind the US and Holland. Looking at M&A, the UK was the second largest dealmaker last year based on insight from TTR data, a provider of corporate intelligence, with 41 concluded transactions. Over the last 10 years, total incoming M&A volume was worth around $25billion, with over 200 deals, based on this author’s proprietary market tracking. That is, on average, $2.7billion in dealmaking volume each year. The top sectors have been financial services, technology and O&G. For instance, BP, Souza Cruz and Three UK, have made significant acquisitions in the country over the last few years.

This year British investment fund Actis — historically very active in Brazil — concluded the acquisition of 11 data centres throughout Latam from the Spanish group Nabiax for around $500 million. Last year, the fund also invested around R$700million to acquire 10% of Omega Energia, a leading Brazilian clean energy group. Education M&A has also been growing. Since 2018, British education giants Cognita and Inspired have been active in acquiring local school groups as the primary and secondary education segments consolidate in the country. The 2022 UK-Brazil Double Taxation Agreement should strengthen bilateral commercial links even further, when it is eventually implemented.

M&A frenzy

Cheaper public company valuations spill-down into the broader private equity and M&A universe. Transaction EBITDA multiples in the Brazilian middle-market segment range typically range between 5-7x, against around 10-11x seen in US markets, according to Capstone Partners data. Furthermore, if interest rates start to fall then dealmaking will become more viable. After a record haul of IPOs in 2021, last year didn’t see any, as risks mounted. Thus M&A activity could be a more promising bet in 2023. Indeed, some of the largest M&A operations last year were public on public, such as Rede D'Or acquiring SulAmérica and Fleury merging with Hermes Pardini in mega health deals and BR Malls and Aliansce merging in the retail mall segment. And cross-border M&A in Brazil has totalled almost $290billion over the last two years so it’s already at a relatively high base.

Consolidation is a major investment theme in Brazil as many industries are more fragmented than in comparable markets. In the last few years, we have seen acute consolidation at play in the health, financial services, logistics, supermarkets and technology sectors. Logistics M&A for instance has grown by around 50% each year. Leonardo Santamaria, investment analyst at Suno Research, believes “the great value of Brazilian equity, both in listed and private markets, is in the long term”. Having a longer cycle helps normalise volatility.

As João Caetano, MD of Brazilian cross-border M&A firm, Redirection International, argues “Even with the uncertainties in the Brazilian political and economic scenario, 2022 was a robust year in terms of M&A transactions. Some sectors that performed well should continue to grow in the coming years, such as agribusiness, biotechnology and education. Brazil is too big a country to ignore, and there is a lot of interest from global buyers.” The combination of low valuations with strong market growth in multiple sectors explain why Brazil is sucking in foreign capital. After all, medium-term nominal economic growth forecast at 5.7% a year. The country is well worth an informed look or, as Benjamin Franklin once said, "an investment in knowledge pays the best interest”