Interview with Juan Carlos Jobet, Chile's Minister of Energy and Mining

The minister in charge of Chile's powerhouse commodities sector explains why his country will become a Latin American leader in renewables...

LatAm INVESTOR: Chile has seen massive solar power growth in recent years; is the market now saturated?

Minister Jobet: The solar power market will continue to grow in the following years in Chile. However, we must habilitate new technologies that allow us to continue incorporating solar photovoltaic (PV) to the grid without it saturating. In order to continue incorporating more PV capacity we need greater demand during daylight hours, promoting consumption in these hours in order to make it economically attractive to existing or future large consumers – for example green hydrogen producers.

Moreover, we are promoting the deployment of energy storage systems, which will allow us to use that excess solar energy during the day at night. We are also seeing an important space in the market for Concentrated Solar Power (CSP) towards the end of this decade, which will allow us to harness our unmatched solar resources without the challenges described before, which are inherent to solar PV.

LAI: What innovation or R&D initiatives will Chile use to become a regional leader in hydrogen?

MJ: We are currently seeing a number of initiatives rising from local academia, in coordination with the private and public sectors, to tackle challenges around the application of green hydrogen in hard-to-electrify and therefore hard-to-abate industrial processes, along with the development of such projects. Some of them are more focused on industrial piloting and project co-development, while others focus on engineering novel materials and processes for hydrogen applications in synthetic fuels production, copper smelting, steel production, among others.

In this century the world is reconfiguring its 'map' towards the leadership of countries with greater renewable resources

The government has a strategic role in promoting these innovation and R&D initiatives in order to foster value addition on this emerging industry. We have established a Clean Technologies Institute – an innovation platform with public funding of up to $193million over the next 10 years - to tend to the technology and innovation demands of the emerging green hydrogen and derivatives industry.

LAI: Green hydrogen is one of the most expensive renewable energy sources technologies; why is it a central part of your energy policy?

MJ: Chile has such abundant renewable resources that it won’t be able to consume them all locally in the form of electricity. Our estimations show that we have a renewable potential for over 80 times the current installed capacity of our power grid. Therefore, we must find ways in which to harness these resources to either export them elsewhere or use them locally in applications that are difficult to electrify. That is where green hydrogen comes in, as the most versatile energy vector, that may be used as an emissions-free fuel or to produce green commodities that derive from it, such as ammonia, methanol, synthetic fuels, among others.

Its main cost component is renewable energy and Chile has a comparative advantage in that domain, since not only do we possess abundant resources but also some of the best quality, yielding unmatched capacity factors and therefore unprecedented costs of energy production within our territory. This is why we are betting to lead in the green hydrogen economy, which is building global momentum as nations realize that its versatility will be critical to achieve their emissions reductions towards net zero.

LAI: Where are the investment opportunities in Chilean renewable energy?

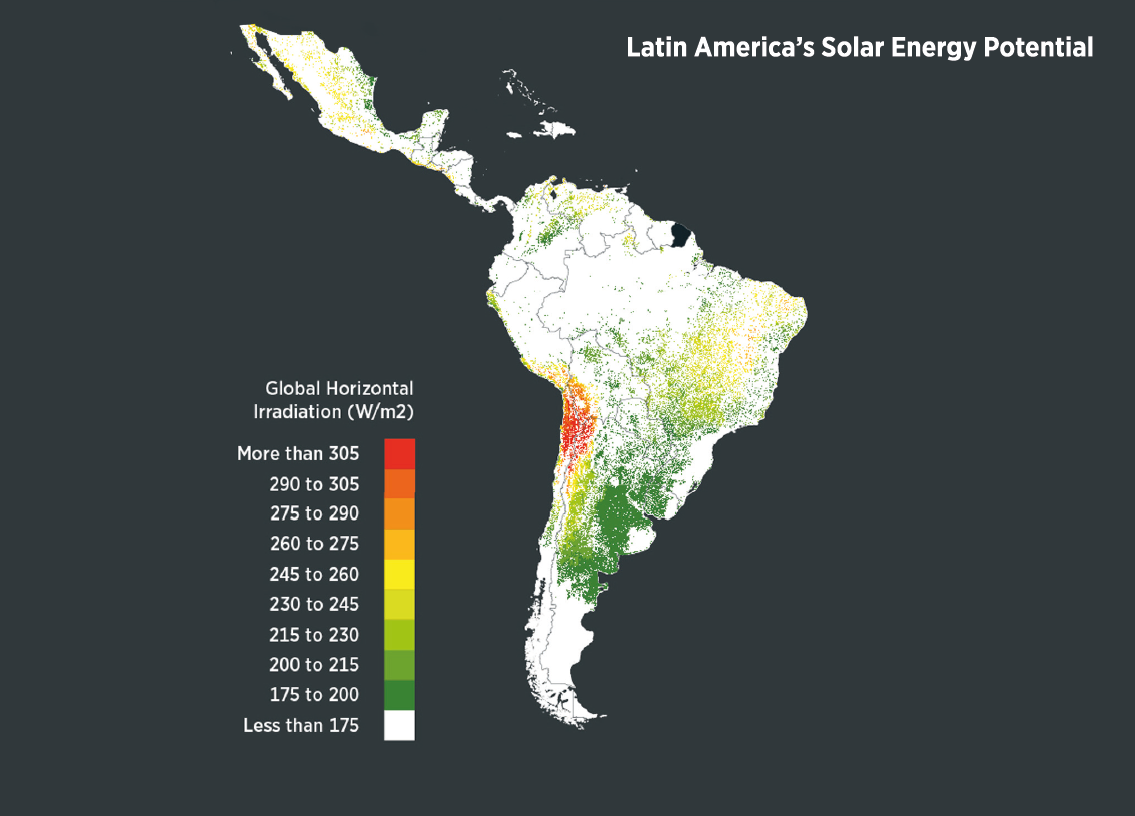

MJ: Our country has been blessed with renewable resources along its entire territory, which is more than 4,000 km long, covering diverse latitudes and climates. In the center-south, rainy climates give way to strong winds, while the Andes Mountains provide a great number of river basins. However, Chile’s best non-conventional renewable resources lie in its territory’s extremes.

The Atacama Desert in the north counts on the highest levels of solar irradiance in the world, yielding capacity factors for solar PV projects of up to 37%. The Antofagasta Region has been the preferred destination for renewable energy investment in recent years, possessing not only unmatched solar irradiance but also strong winds in the commune of Taltal. The Magellan Region, in southern part of Patagonia, holds the strongest and most persistent winds within our country, yielding capacity factors of up to 75% for on-shore wind turbines, which is completely unprecedented.

LAI: Chile has some of the largest lithium reserves in the world but its production remains relatively low; what will you do to increase lithium production?

MJ: This is an important opportunity for Chile, since we hold more than half of the global reserves and forecasts show that demand for lithium will vastly exceed supply, as one of the critical minerals for the global energy transition. We are working to promote exploration for new production projects in a way in which we can ensure the incorporation of new players to the market. The goal is to boost competition and production output in an environmentally friendly way, with projects that contribute to communities located where the mining takes place.

LAI: The world needs copper for the energy transition yet mining is a major source of GHG emissions; how will you minimise its environmental impact?

MJ: We are pleased to witness that during these last days a number of the world’s largest mining companies have set carbon neutrality commitments by 2050. Many of them have operations in Chile and we have seen good progress. Companies have increasingly switched their energy supply contracts from fossil sources to renewables, allowing for the development of several large-scale renewable energy projects in the past years. We expect that 63% of the mining sector’s total energy demand will come from renewables by 2023.

However, other mining operations such as heavy transport trucks are fossil-intense and we must work, along with the industry, towards decarbonizing those processes. Incorporating green hydrogen fuel cells to power these heavy vehicles is an option that is currently being worked on by the industry, that would have a significant impact on reducing the industry’s total GHG emissions.

LAI: Could a radical, left-wing government derail the country’s renewable energy potential?

MJ: The development of the Chilean energy sector has broad political support. We have built that support for hydrogen too. As Government we have worked to lay the foundations of this new industry, confident and hopeful that the administration that assumes this challenge will give continuity to this great national project, that has the potential to transform the country's productive identity in just one generation. In fact, most of the candidates’ campaign platforms have green hydrogen as a priority, which is a strong signal.

Additionally, the update of the Chilean National Energy Policy 2050, incorporates for the first time the topic of green hydrogen, recognizing it as a unique opportunity to reduce emissions from the country's main productive sectors. The goal is that green hydrogen will represent 70% of the non-electrical energy uses by 2050.

LAI: What will Chile’s renewable energy sector look like in 2030.

MJ: In the 20th century, countries that produced fossil fuels -particularly oil- were protagonists both commercially and geopolitically. In this century the world is reconfiguring its “map” towards the leadership of countries with greater renewable resources and comparative advantages to produce carbon-neutral goods and services.

Carbon neutrality (CN) and “green” attributes of commodities and final products constitute a paradigm shift in international markets. Chile must take advantage of it, as a country with tremendous resources and a robust strategy to become carbon neutral.

This is a unique opportunity for Chile to position itself globally as a clean investment destination and carbon neutral provider through the export of its vast clean energy potential in the form of emerging commodities such as green ammonia, synthetic fuels, green copper and steel, among others. In this way, we will assume as a country a productive carbon neutral identity.