Latin America's Catastrophe Problem

Latin America is subject to a wide range of natural catastrophes with severe economic consequences. LatAm INVESTOR looks at how it impacts investors...

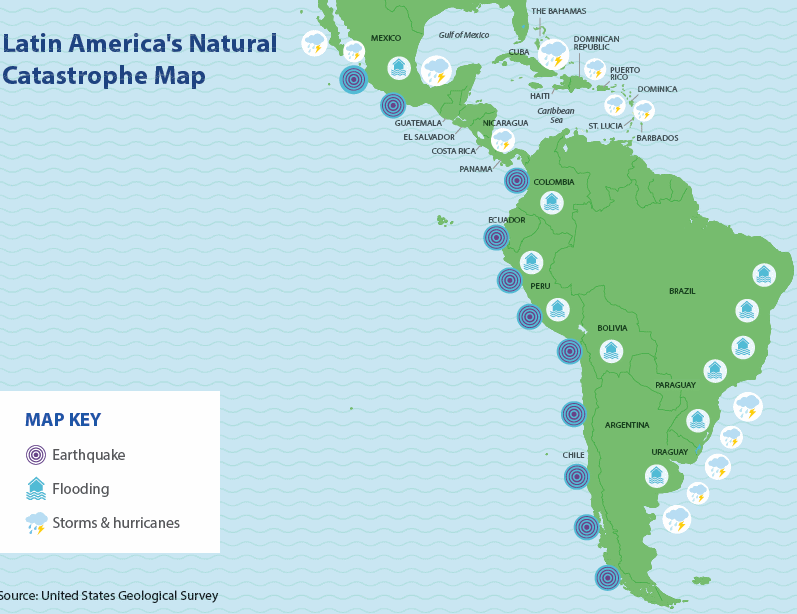

What happened?

More than 650 people have died in an earthquake that struck Ecuador’s Pacific coast on Saturday 16th April. With a magnitude of 7.8, it is the most powerful quake to strike the country since 1979 when at least 600 people were killed. Speaking to survivors, President Rafael Correa said that the economic impact “could be huge”. Approximately 10,000 troops and 4,600 police were deployed in response to the quake; 25,000 people are being housed in temporary shelters.

Natural disasters of this scale are not uncommon in Latin America. In 2010, a magnitude 8.8 quake struck Chile causing an estimated $30bn in damage; the earthquake that struck Haiti in the same year led to over 100,000 deaths. Mexico City was famously struck by a magnitude 8 quake in 1985 that left 5000 dead and an estimated $5 billion in damage. It’s not just earthquakes that are common in Latin America: hurricanes, volcanic eruptions and floods are a constant challenge to governments in the region.

Why does it happen?

Much of the western coast of Latin America is part of the Pacific Ring of Fire, an area in the basin of the Pacific Ocean where large numbers of earthquakes and volcanic eruptions occur. The unique tectonic structure is the cause of around 90% of the world’s earthquakes – and many occur in Latin America. Additionally, Central America, the Caribbean and parts of Mexico are pounded by hurricane season. Every year between May and December hurricanes and tropical storms form off the Pacific and Caribbean coasts and move across land.

Finally, Latin America suffers from the El Niño phenomenon, which disproportionately affects Latin America compared to the rest of the world. The irregular warming and cooling of the Pacific Ocean causes higher wind speeds in Mexico and more extreme temperatures, as well as rainfall, in South America. Its effects can be devastating – the 1997/8 El Niño caused $2billion of property damages in Peru through flooding and landslides. Fishery exports dropped 87% as fish migrated away from the Peruvian coast as a result of disruptions to the water temperature. In short, Latin America is particularly vulnerable to natural disasters due to its geographical location, large urban population, and heavy reliance on the primary sector. So it’s no surprise that World Bank estimates that nine of the world’s top 20 countries most exposed to disaster-led economic impacts are in the Latin America.

What’s the economic cost?

The economic cost for Latin America depends on the scale of the natural disaster, the preparedness of the region struck and its population or industrial density. According to the World Bank, natural disasters cost the Latin American region $2billion annually. This is partly due to geographical misfortune, and also to a lack of investment in preventative measures and emergency responses.

The costs are so high in Latin America because of the high population density of cities: 80% of people in the region live in urban environments that often lack the correct drainage systems and building structures to resist natural disasters.

Measuring the economic costs of natural disasters is difficult. The World Bank predicted that Colombia has paid out more than $7.1billion over the last 40 years. Colombia’s government estimates that a huge quake of 8.5 or more on the Richter scae, which is due once every 250 years could causes losses to public assets and housing totalling more than $35 billion – around 8% of GDP. One such mega quake struck Chile in 2010. Measuring 8.8 on the Richter scale it was one of the largest earthquakes ever recorded. Damages to the economy were estimated at around $15billion as buildings were flattened and tsunamis battered ports. Chile was lucky that the quake did not strike in the capital Santiago, where the human and economic toll would have been worse. Chile was also in a much better position to protect itself economically, as it had an $11billion sovereign wealth fund at its disposal for rebuilding efforts. The cost to Ecuador of its recent quake is expected to be around $3billion, which is 3% of the country’s GDP. The lower cost is down to the fact that Ecuador is a poorer country, while the quake hit rural areas and did not cause serious damage in Guayaquil or Quito, the country’s principal cities.

How can Latin America protect itself?

Investment in forecasting natural disasters and limiting their impact is the most effective policy. Installing early warning systems gives governments and citizens the vital time they need to react according. On top of this, evacuation drills and education in schools and the workplace about natural disasters will lead to a citizenry that is better prepared. When it comes to dealing with the natural disasters themselves, urban planning and infrastructure improvements reduces the initial impact, while improving drainage systems cuts the likelihood of flooding and the threat of diseases spreading after any event.

The importance of preparation was extremely evident in 2010. Chile suffered a quake 500 times more powerful than that which struck Haiti in the same year. However, the death toll in Chile was 800 compared to more than 160,000 in Haiti. Much of this came down to vastly superior infrastructure and disaster management in Chile compared to Haiti.

Latin America could learn from Japan, which is on the other side of the ring of fire. In Japan high-rise buildings are designed to sway rather than shake and buildings are fitted with underground shock absorbers that allow the structure to move with, rather than against, the earth. Moreover, every Japanese person is drilled on how to react to quakes – the emergency response is calm and precise. Latin American governments need to replicate Japan’s natural disaster policy and invest in modernising its infrastructure and educating its population.

What about insurance?

Insurance against natural disasters is uncommon for Latin American governments. Credit lines activated by natural disasters, as well as government spending, make up the traditional funds for disaster response. The World Bank offers a Catastrophe Deferred Drawdown Option (Cat DDO) that provides immediate liquidity in the case of a disaster. Costa Rica, Guatemala, El Salvador and Colombia have all tapped into this fund to respond to earthquakes and irregular weather threats. Ecuador has activated $600million from multilateral lenders to respond to the current crisis.

However, there are some signs of change. The Mexican state issued catastrophe bonds in 2009 and 2012 to provide coverage against earthquakes and hurricanes. Facilitated by the World Bank’s MultiCat Programme, Mexico locked funding for disaster relief prior to the event happening, reducing pressure on the public finances. Uruguay has insurance against the impact of low rainfall on its hydroelectric sector and Peru in 2014 took out insurance for US$ 156 million against crop damage. There is a growing belief across the region that governments should follow the lead of the private sector and protect their assets against natural disasters instead of relying on emergency credit lines.

It is much more common for the private sector to have insurance. Insurance companies paid out around $7billion following Chile’s 2010 quake, which helped pay for the rebuilding effort. Companies in Peru involved in the construction of highways, docks and airports use insurance to protect their projects against natural disasters.

Is this realistic in Latin America?

Insurance penetration in Latin America has traditionally been very low due to weak property rights, low financial inclusion and stuttering GDP growth. This changed following the dramatic rise of commodity prices after 2002. A new middle class has emerged, and with it, a heightened interest in insurance. Figure 1 shows the insurance spending as a share of GDP. Spending on insurance has risen across much of Latin America.

Further increases in demand for insurance are expected. The industry in Peru has grown at an annual rate of 14.6% for the last five years, but it still lags far behind that of Colombia and Chile. A more supportive regulatory environment is also driving demand. . Access to the Latin American insurance market to international companies has not always been straight forward. The Brazilian reinsurance market was opened up to international competition in 2008 after the state monopoly was dismantled. By 2020, 85% of the reinsurance market will be open to foreign insurers. UK plc could also have a role in helping Latin America protect itself from natural disasters. British insurers are global market leaders and want to access this lucrative market by offering reinsurance or insurance directly.